Stablecoins for Banks: What, How, and Why

- Marcia Klingensmith

- Sep 25, 2025

- 2 min read

Stablecoins are no longer a fringe experiment. With the U.S. GENIUS Act and Europe’s MiCA framework now in force, stablecoins have moved from the “crypto wild west” into the regulated payments stack. For banks, this shift isn’t theoretical — it’s strategic.

The question isn’t if stablecoins matter, but where they fit in your modernization roadmap.

Why Stablecoins for Banks Matter

Banks face three realities today:

A competitive threat: Fintechs and wallets are already monetizing stablecoin flows for cross-border payments, gig economy payouts, and programmable disbursements.

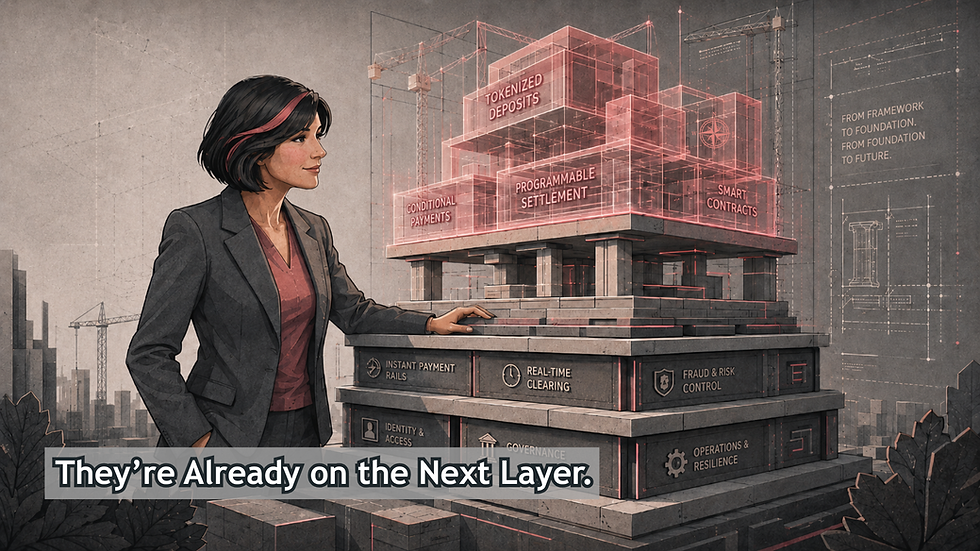

A new rail: Stablecoins operate 24/7, settle in seconds, and can be programmed for conditional payments.

A regulatory obligation: If you issue, hold, or partner, you’re now operating under emerging frameworks like GENIUS and MiCA.

Stablecoins for banks are not about becoming a “crypto shop.” They’re about staying relevant in a world where clients are already exploring faster, cheaper rails.

Stablecoins vs. FedNow and RTP

Stablecoins differ from domestic instant rails like FedNow and RTP in three key ways:

Global reach → Stablecoins can move value across borders natively.

Programmability → Smart contracts enable milestone-based, escrow, or automated disbursements.

Custody choices → Banks must decide whether to act as issuers, custodians, or orchestrators.

For many institutions, the opportunity lies in multi-rail orchestration: using stablecoins alongside FedNow, RTP, card push, and wires — selecting the best rail based on speed, cost, risk, and compliance.

De-Risking Adoption with SAFE to SEND™

My SAFE to SEND™ framework gives banks a structured path to evaluate and adopt stablecoins without adding unnecessary risk.

SAFE™ (Settlement, Authentication, Fraud & Exposure, Economics) ensures you assess reserves, compliance obligations, and fraud controls.

SEND™ (Strategize, Explore, Narrow, Design) helps you identify high-fit use cases, run board-ready pilots, and commercialize quickly.

The result? A safe, monetizable entry point into stablecoins for banks that aligns with your broader modernization strategy.

What’s Next

If your institution is exploring stablecoins for banks, you don’t need another whitepaper. You need a clear path forward.

📥 Download the SAFE™ Risk Scorecard to baseline your readiness.📞 Book a complimentary discovery call to see how SAFE to SEND™ can help your institution adopt stablecoins safely, unlock new revenue, and future-proof your payment rails.

Or, dive deeper into the details:📖 Read my full article on Substack: Stablecoins 101 for Banks

Comments