The Hidden Risks of Staying Receive-Only

- Marcia Klingensmith

- Sep 11, 2025

- 2 min read

Why Receive-Only Inaction Is the Riskiest Move for Financial Institutions Today

Most banks and credit unions have already gone live on instant payments rails like FedNow or RTP. But here’s the truth: many are still stuck in receive-only mode.

On paper, that seems safe. You can say you’ve “checked the box” on modernization, avoid the complexities of Send, and buy time. But beneath the surface, receive-only isn’t safety — it’s exposure.

Here are five blind spots most leadership teams overlook:

Competitive Blind Spot

Fintechs, wallets, and ERP-driven payouts are monetizing Send flows right now. That means every delay costs you not just revenue, but relevance.

Action Check: Which three flows in your market are fintechs already taking from you

Liquidity Blind Spot

Receive-only doesn’t eliminate liquidity risk. It shifts it. Without Send, treasury loses the ability to balance inflows and outflows in real time — leaving you reactive instead of resilient.

Action Check: Could you withstand a weekend stress test without Send?

Regulatory Blind Spot

Global frameworks like the GENIUS Act (U.S.), MiCA (EU), and DARE (Bahamas) are moving faster than most boards expected. Staying on the sidelines means missing the chance to build trusted guardrails before they’re mandated.

Action Check: Do you know how your institution would comply if Send went live today?

Data Blind Spot

ISO 20022 is more than compliance — it’s monetization. Receive-only keeps your data passive instead of powering dashboards, reconciliation, and fraud detection that customers increasingly expect.

Trust Blind Spot

Clients won’t wait. Corporate treasurers, consumers, and fintech partners will migrate to those offering faster settlement. The longer you delay Send, the more trust you erode.

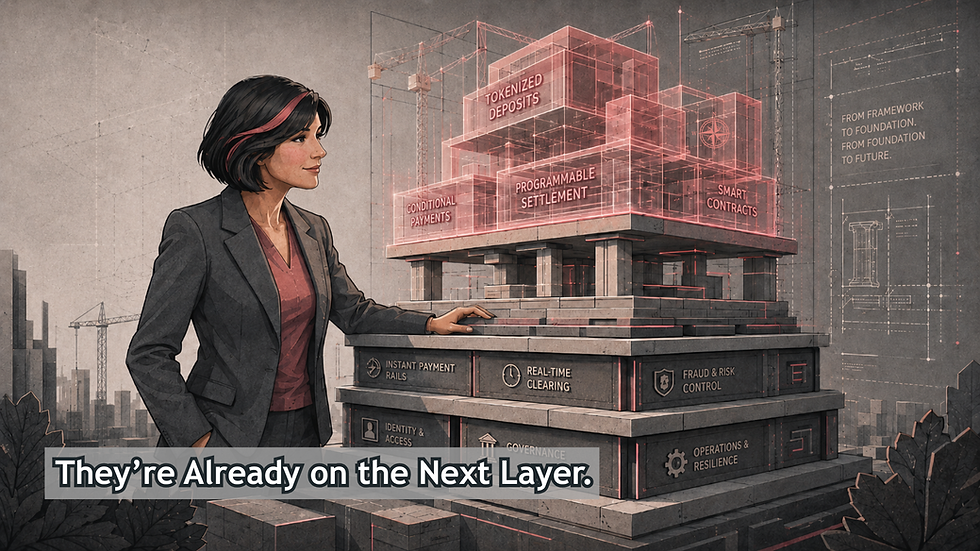

From Blind Spots to a Board-Ready Path

Inaction guarantees deposit erosion, reputational decline, and missed revenue. Receive-only is not neutral — it’s a liability.

The good news: risk can be managed. Through the SAFE to SEND™ framework, financial institutions can build a board-ready plan to:

Launch low-risk, high-benefit use cases like payroll and insurance payouts.

Model liquidity and compliance exposure with confidence.

Monetize data and position for the programmable future.

🔗 Want the full breakdown of each blind spot, plus a practical checklist to bring into your next leadership meeting?

Read the full article on my Substack: The Instant Edge by the Payments Maven™

Comments